All Categories

Featured

Table of Contents

A PUAR allows you to "overfund" your insurance coverage right approximately line of it ending up being a Modified Endowment Agreement (MEC). When you utilize a PUAR, you quickly raise your cash worth (and your survivor benefit), thus enhancing the power of your "financial institution". Further, the more money worth you have, the better your rate of interest and dividend settlements from your insurance provider will be.

With the surge of TikTok as an information-sharing system, economic suggestions and strategies have actually found an unique method of dispersing. One such strategy that has actually been making the rounds is the unlimited financial idea, or IBC for short, garnering endorsements from celebrities like rap artist Waka Flocka Flame. Nevertheless, while the technique is presently prominent, its roots trace back to the 1980s when financial expert Nelson Nash presented it to the world.

Is there a way to automate Bank On Yourself transactions?

Within these policies, the cash money value grows based upon a rate set by the insurance provider (Infinite Banking). As soon as a considerable cash value accumulates, insurance policy holders can obtain a cash money worth car loan. These fundings differ from conventional ones, with life insurance serving as collateral, implying one can shed their coverage if borrowing excessively without sufficient cash value to sustain the insurance policy expenses

And while the appeal of these plans appears, there are innate limitations and threats, requiring attentive money value monitoring. The strategy's authenticity isn't black and white. For high-net-worth people or business owners, particularly those using methods like company-owned life insurance policy (COLI), the advantages of tax obligation breaks and compound growth can be appealing.

The attraction of boundless financial doesn't negate its difficulties: Price: The fundamental requirement, a long-term life insurance policy plan, is costlier than its term counterparts. Qualification: Not everyone receives entire life insurance as a result of rigorous underwriting processes that can leave out those with certain wellness or way of life conditions. Intricacy and risk: The detailed nature of IBC, paired with its dangers, may deter several, particularly when less complex and much less risky options are offered.

What are the risks of using Cash Flow Banking?

Assigning around 10% of your regular monthly income to the policy is simply not feasible for most individuals. Component of what you read below is simply a reiteration of what has actually currently been claimed over.

So prior to you obtain right into a circumstance you're not planned for, recognize the following first: Although the idea is commonly marketed as such, you're not really taking a financing from yourself. If that held true, you wouldn't need to settle it. Instead, you're borrowing from the insurer and have to repay it with interest.

Some social networks blog posts advise utilizing cash value from entire life insurance policy to pay down bank card financial debt. The idea is that when you repay the loan with rate of interest, the amount will be returned to your financial investments. That's not how it functions. When you pay back the finance, a section of that passion mosts likely to the insurance firm.

For the initial numerous years, you'll be repaying the compensation. This makes it very challenging for your policy to gather worth throughout this time. Entire life insurance policy costs 5 to 15 times much more than term insurance policy. Lots of people merely can not afford it. Unless you can pay for to pay a couple of to several hundred dollars for the next decade or more, IBC won't work for you.

How secure is my money with Financial Independence Through Infinite Banking?

Not everyone must rely solely on themselves for financial safety and security. If you need life insurance, here are some valuable tips to take into consideration: Take into consideration term life insurance policy. These policies offer insurance coverage throughout years with significant economic commitments, like home mortgages, trainee financings, or when taking care of little ones. Make sure to search for the best rate.

Envision never having to fret concerning bank fundings or high interest prices once again. That's the power of unlimited financial life insurance coverage.

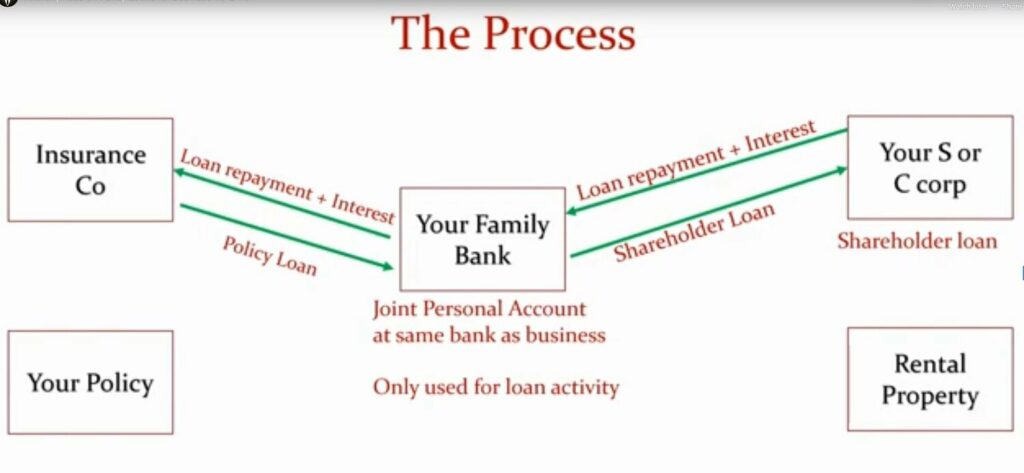

There's no set finance term, and you have the freedom to choose the payment timetable, which can be as leisurely as repaying the funding at the time of death. Policy loans. This versatility includes the servicing of the car loans, where you can select interest-only repayments, keeping the financing balance level and convenient

Holding money in an IUL dealt with account being credited passion can commonly be better than holding the money on deposit at a bank.: You've constantly imagined opening your own pastry shop. You can obtain from your IUL policy to cover the preliminary expenses of leasing a space, purchasing equipment, and employing personnel.

How do I leverage Self-financing With Life Insurance to grow my wealth?

Individual lendings can be acquired from standard banks and lending institution. Right here are some essential factors to think about. Bank card can give a versatile way to obtain money for really short-term durations. Nevertheless, obtaining money on a bank card is normally extremely expensive with interest rate of interest (APR) usually getting to 20% to 30% or more a year - Whole life for Infinite Banking.

{kind=link}

Latest Posts

Your Own Bank

Bank On Yourself Review

Cash Flow Banking Strategy